In Part 1 of this series we saw that the European Union is dependent on Russia for a large proportion of its energy: 46% of coal, 38% of gas, and 23% of oil. These fossils are used to keep the lights on, power industry, heat homes, and move people and goods. It’s a big dependence and one that is becoming more scary and less palatable with each day of Russian bombing of Ukrainian cities and civilians. And it runs both ways: these pipelines are funding Russia’s war machine (EU energy imports accounted for 4% of Russia’s GDP in 2020[1,2]) and Russia can threaten to turn off the tap in wintertime when people need heating the most. What can Europe do to lessen this dependence?

I’ll spoil the plot in case you’re busy: This is a scary situation, but there is a way to decrease Europe’s reliance on Russia. It’s not ideal, it’s not very clean, but it sure beats World War III.

The fossil fuel trade is a huge and slow moving network. Fuel is not traded on the spot, but mostly through titanic international supply agreements. As ‘spot’ purchases are subject to availability and price fluctuation, countries look to futures markets to secure supply more affordably. Another factor is the cost of scale: a nation needs to be pretty sure it wants to keep burning petrol, for example, before it builds another refinery.

And then we have production. There are still vast reserves of fossil fuels around the world, but the rate of extraction is (thankfully for global warming) quite slow. Since the amortisation (paying off) of the expensive facilities that move, refine, and burn fossil fuels takes many years, extraction is meant to closely track demand. And that turns the trade agreements that move fossil fuels into a zero sum game: for example, if the USA wanted to provide more gas to Europe, it would have to supply less to other partners, say, Japan. Keep that in mind, it will become important later.

Desperate measures

Keeping in mind this zero-sum trading entrenchment, let’s get back to our theme of what Europe could do to get off Russian energy imports.

We spend our fuel on a plethora of activities but a lot of it goes into electricity generation. Given the centralisation of generation into power plants, this makes electricity a good starting point—it’ll be an easier accounting exercise than figuring out how to change consumption at individual homes, businesses, and industries (give me a couple of days to write Part 3!).

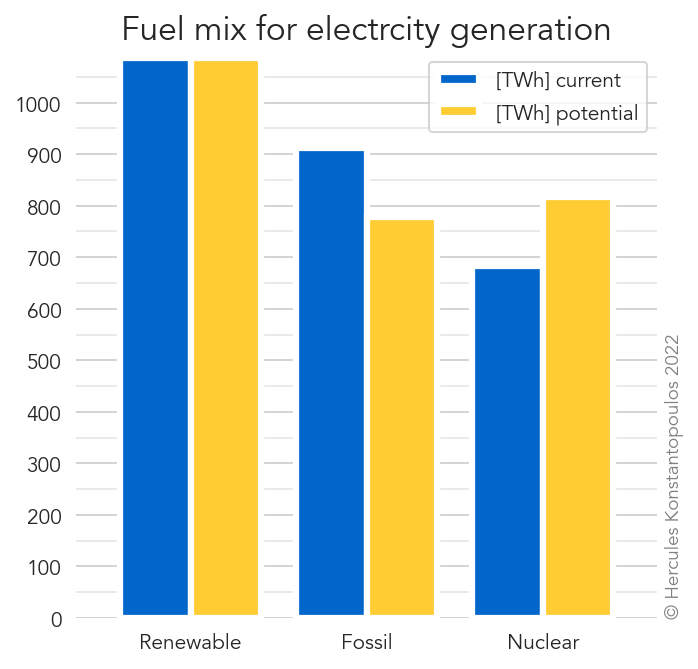

In Part 1 I plotted the fuel mix of electricity production in Europe. Let’s have another look at that:

See that (red) segment third along on the electricity bar? That’s nuclear. I am sure to lose a few environmentalist friends in the coming seconds… I want to look at how much of that gas imported from Russia we can offset by boosting nuclear electricity generation.

Europe has a long history of generating electricity in nuclear plants. It’s no surprise: nuclear energy is vastly superior than combustion. The energy contained in one kilogram of gas is 53.6 MJ (Mega-Joules); one kg of Plutonium contains 84 million MJ. Even after conversion to electrical energy, that’ll be 21 MJ vs 31 million MJ.

Nuclear is expensive, however, which often leads countries to scale down operations. Sweden decided to save the pennies by decommissioning 4.1 GW of its total 11 GW[3,4]. A more important factor in that decision tends to be safety, or at least, the perception of safety. After the Fukushima disaster, Germany opted to begin decommissioning its fleet of nuclear plants. In May 2011 it had 14 operating units in 12 stations[5]. Now it has three stations (each with a single unit) that are meant to be shut down this decade. Germany’s nuclear capacity reduced from 20.5 GW to 4 GW, and is slated to go away quite soon. Or, at least, it was: after the 28 February invasion it was reported that Germany may slow down that closure plan.

I propose to take a drastic step in the opposite direction.

Shuttered (but not yet dismantled) plants can be safely brought back online. Yes, there is danger in nuclear energy, but there is also considerable danger in Mad Vlad setting his nuclear war units to combat readiness. Same atoms, different vessel.

Let’s tally what we have:

- Turn on the units in Sweden that were shuttered for financial reasons: 4.1 GW.

- Turn on units and plants in Germany that were shuttered after Fukushima: 16.4 GW.

- To keep it simple, offset just natural gas used for electricity generation.

That resulting 20.5 GW will be subject to an efficiency factor: given their risky nature, nuclear plants require maintenance to ensure safety. It is hard to gauge the proportion of up-time, so I derived a pan-european average of units currently in operation[6]. That’s a surprisingly high 74%. Multiply 365 days by 24 hours, by 20.5 * 109 Watts, and apply that 0.74 factor, and we get 133,565 kWh of idle nuclear capacity.

Let’s remove that from electricity currently generated with gas:

The set of blue bars on the left show the current mix of EU electricity generation: renewables are followed by fossils, and then nuclear. In the nuclear scenario renewables are unchanged, but we offset fossil generation with nuclear energy, thus lessening the EU’s dependence on Russian gas. Just turning on units in two countries with impeccable safety records we can offset 14% of thermal (fossil) generation.

More importantly, what proportion of Russian gas imports does this remove?

Maths warning! We can express gas in terms of gross calorific value, apply a thermal-to-electric conversion factor of 39%[7], and compare Terra-Joules for each source. For nuclear, we multiply our 20.5 GW by seconds in a year and the nuclear power plant efficiency factor of 74% (derived above) to get Joules.

| Generation method | Annual energy output |

|---|---|

| Nuclear | 481,000 TJ |

| Fossil gas | 2,280,000 TJ |

Powering shuttered nuclear units in Germany and Sweden can offset 21% of Russian gas imports.

The big caveat here is localisation. We have just a few locations in Northern and Central Europe and transporting energy over long distances comes with losses. So this is an upper limit.

But wait, there’s more! As an aside, let’s calculate what CO2e reduction we can expect from those TJs of nuclear.

To get an emissions intensity we need to figure out what kind of plant is prevalent in the EU: open cycle (OC) or combined cycle (CC). From this Eurostat dataset it looks like a ten-to-one balance of CC to OC, which is great because they are heaps more efficient (new tech can get to 60%; Smil, 2017) and less polluting. The median unit-emissions of a combined-cycle plant are 751 grams of CO2-equivalent emissions per kWh[8]. Remember, we are offsetting 133,565 GWh.

The nuclear offset option would prevent the release of 100 million tonnes of CO2e from the atmosphere each year. This amounts to 3% of overall EU emissions, and 5% of the 2030 emissions reduction goal. Frankly, this sounds more like a winning option than a desperate measure!

Gas in another phase

Gas either flows through pipelines or is liquefied for transport over oceans. One topic that’s been discussed a lot in the past week is the potential of liquefied natural gas (LNG) to replace what is currently flowing into Europe through the Russian pipelines. The Economist published a neat summary and these clever folk at Bruegel dove deeper with some models.

In a nutshell, this is where the whole zero-sum trading game comes back to bite us. But just because break fees and exit clauses from existing agreements with non-EU partners are expensive, that shouldn’t stop us from hypothesising! It is wartime after all, and the financial cost of it spreading further (let alone the horrors of further escalation) would be titanic.

To build a toy model of offsetting pipeline gas with LNG we need two basic building blocks: production and export capacity of available LNG; and ability to re-gasify at the point of consumption.

Europe has plenty of idle regasification capacity in its current terminals (running at 45% according to that Economist summary), but not really in the right places. Turning LNG into gas in the outskirts of Athens does nothing to feed a combined-cycle plant near Wroclaw. Still, let’s run the numbers and see where they take us.

LNG production

Without going into tremendous detail, there is plenty of LNG around. But it is tied up in various contracts, increasingly in Asia. The United States, currently a big provider of natural gas to Europe, is the third biggest producer in the world, after Qatar and Australia. But according to the Energy Information Administration (EIA), a lot of liquefaction capacity is being added in 2022, of order 2.4 billion cubic feet per day (in regasified units). According to the timeline on the report a bunch of this capacity is meant to be installed already.

President Biden has signalled that his country is not able to bridge the Russian gas gap, but they can help the EU source elsewhere. Hypothetically though, what if the USA directed all that newly added capacity to Europe? How much LNG would that deliver to European terminals?

Multiplying by 365 days to get an annual (nominal) production, and converting to million cubic metres per day, we get 24.5 billion m3. The nuclear offset exercise above left us with 116 billion m3 meaning that this hypothetical redirection of increased US gas would deliver 20% of that remainder. That’s pretty good. Let’s put that all together.

With two quick measures we can potentially dump 40% of Russian gas imports. Let’s not forget that there are two sides to a trade: if this terrible invasion escalates further, Russia could just turn off the tap to counteract European military aid to Ukraine. We need to be preparing immediately.

Swapping trade parners

Nuclear and LNG provide pretty neat illustrations of how to offset gas imports. When it comes to other fossils it isn’t as simple to find short-term offsets. Oil mostly feeds Europe’s passenger car fleet, so mitigation could require behavioural change. Coal is used heavily for steel production but also for industrial process heat (e.g., making powdered milk using a cheap coal boiler), which can be electrified and powered with renewables. But that is not something we can achieve in a few months. I’ll get into all of that in the next instalment.

For now, let’s look at sourcing from elsewhere—again, contracts and exit fees apply, so this is hypothetical.

Coal

Having spent seven wonderful years in the coal-loving land of Australia that was the first partner that popped to mind. Australia’s current export volume is 390 Mt of coal (177 Mt metallurgical coal and 213 Mt thermal coal)[9,10]. Let’s focus on black coal.

Just for context and units, Australia’s easily reachable (economic) reserves are 75,428 Mt[10], 1750 times Europe’s annual import of Russian black coal. Let’s hope most of it stays in the ground. Combined annual production of black and brown coal is around 500 Mt, roughly 11 times the RU import into EU.

In this exercise we want to offset roughly 44 Mt of Russian coal imports, which represents 9% of annual production.

(I can’t believe I’m about to suggest that we dig up more turds, but moral inflexibility is a luxury of peacetime. Also, hopefully, this will be a like-for-like substitution, not a net increase in coal burning.)

Is Australia able to ramp up production by 9%? Does it have reserves of extracted coal at the ready?

Oil

Beside Russia, the United States, Norway, Saudi Arabia, and the UK are the EU’s main trade partners in oil. It takes the combined supply of these four countries to add up to Russia’s annual supply (171 million tonnes), so this will not be easy to offset.

As a rule of thumb, what proportion of each partner’s annual production would Europe have to procure to offset Russian oil?

| Country | 2020 production |

|---|---|

| United States | 559,141 kt |

| Saudi Arabia | 458,135 |

| Norway | 84,702 |

| United Kingdom | 46,837 |

The EU would need the equivalent of 15% of production for the US and Saudi Arabia, and 20% of Norway and UK. Saudi Arabia and the United States would be the obvious starting point here. The US as the closest ally, and Saudi Arabia as an existing market liquidity regulator that releases reserves to keep prices in check. What kinds of reserves do they have?

In any case, this much of a ramp-up in production does not quite sound feasible… so I will pencil this in for the next instalment, where we will look at savings through (currently available) technology and behavioural change.

Best laid plans

Let’s refocus: why am I running these numbers? On the back of the humanitarian crisis caused by a belligerent imperialist power we are also facing a potential energy crisis of never-before-seen magnitude. Russia has in recent times weaponised, in trading terms, fossil fuel supplies—RIP the 24 energy retailers that went bust in the UK this past winter. Europe (and the rest of the world) therefore needs a viable deterrent.

I have examined two measures—turning on recently shut down nuclear power plants and replacing piped with liquefied gas—that can swiftly take the EU a significant part of the way toward independence from Russia. Nuclear power is unpalatable but surely preferable to the dire alternatives, even to the most hard-line environmentalists (like me). All this needs to happen very soon, especially given the sluggish nature of fossil fuel trade. Failing to do so could place Europe in an untenable situation of blackouts and freezing apartments next winter, all the while sending SWIFT transfers to the Russian military.

In the next instalment I will look at solutions that take effect on longer timeframes. Environmentalist friends, please stick around: it’ll be a lot of heat pumps and wind farms!

References

[1] GDP of Russian Federation, World Bank.

[2] EU trade with Russia, 2020, Eurostat.

[3] Sweden speeds up nuclear reactors closure ($).

[4] Nuclear power in Sweden, Wikipedia.

[5] Nuclear power in Germany, Wikipedia.

[6] Nuclear power in the European Union, World Nuclear Association.

[7] Tonne of oil equivalent, Wikipedia.

[8] Emission intensity, Wikipedia.

[9] Coal in Australia, Wikipedia.

[10] Coal, Geoscience Australia.

[11] List of countries by oil production, Wikipedia.

One thought on “SWIFT action: Can Europe dump Russian energy imports? (Part 2)”